How Interest Works on a Reverse Mortgage

When it comes to reverse mortgages used for purchasing a new or better suited home, senior buyers ask one question about how interest works on these HECM for Purchase loans more than any other:

“Won’t the interest just eat up everything my home is worth?”

That question deserves a straight answer. And REALTORS who can deliver that answer with confidence earn trust fast.

Here’s the short answer: Interest on a HECM for Purchase works in a way that actually benefits many senior buyers. It operates differently from a traditional mortgage in ways that matter a great deal to people living on fixed incomes. Understanding those differences helps you hold better conversations, set accurate expectations, and serve your senior clients at a higher level.

Let’s walk through it in plain language.

How Interest Works With No Monthly Mortgage Payment Required

This feature surprises most people when they first encounter the HECM for Purchase.

With a traditional mortgage, the borrower makes a monthly payment that covers both interest and principal. The loan balance shrinks over time. Most buyers know that model well.

With a HECM for Purchase, the borrower makes no required monthly mortgage payment. Interest still accrues on the loan balance each month, but the borrower doesn’t have to pay it out of pocket.

That doesn’t mean the loan carries no obligations. Borrowers must stay current on property taxes, homeowner’s insurance, and basic home maintenance. Falling behind on any of those can put the loan at risk. But the monthly mortgage payment that typically dominates a housing budget? The HECM for Purchase removes that requirement.

For a buyer living on Social Security, a pension, or retirement savings, that distinction and how interest works on reverse mortgages changes everything. It often makes a move possible when a traditional mortgage would close the door entirely.

How Interest Works When the Loan Balance Grows Over Time

Want to know how interest works on reverse mortgages? Because the borrower makes no required monthly interest payment, that unpaid interest rolls into the loan balance each month. Pretty simple and straightforward. Lenders call this negative amortization. The balance grows over time rather than shrinking. That’s how interest works on reverse mortgages.

Here’s a simple example. Suppose a borrower starts with a loan balance of $200,000 and the loan carries a 7 percent interest rate. In the first year, approximately $14,000 in interest accrues. With no payment applied, the balance climbs to roughly $214,000. The following year, interest accrues on that larger balance. And so on.

Over 10 or 20 years, the balance can grow substantially. That surprises some borrowers and their families when they first see the projections.

But reverse mortgages and how interest works solves a real problem. The program trades a growing balance for the elimination of a required monthly payment. HUD-approved housing counseling, which every borrower must complete before moving forward, walks clients through exactly how this product can help and how interest works. Nothing about it stays hidden.

The loan doesn’t come due until the last borrower sells the home, moves out permanently, or passes away. Until one of those events occurs, the borrower stays in the home and makes no required repayment.

Clients who understand this before they sign anything rarely feel blindsided later. You become the professional who prepared them well.

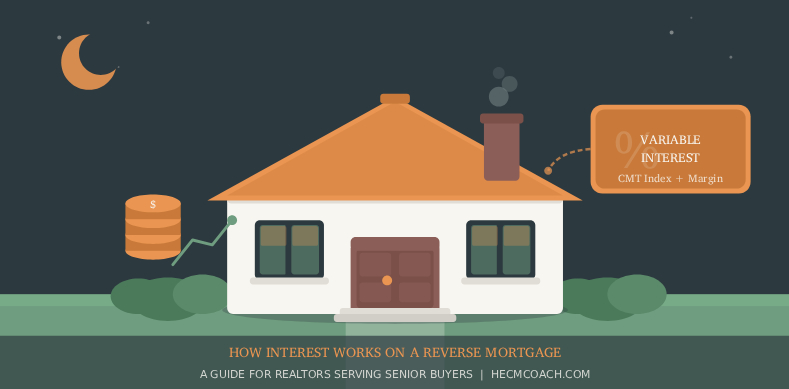

The Variable Interest Rate on a HECM for Purchase

HECM for Purchase loans carry a variable (adjustable) interest rate. A fixed-rate HECM does exist, but it applies to a different loan structure that delivers a lump-sum payout to the borrower. Since the HECM for Purchase doesn’t work as a cash payout, the fixed-rate product doesn’t apply here.

The variable rate on a HECM for Purchase combines two parts that go into how interest works: a benchmark index and a lender margin.

HECM lenders currently use an index called the CMT, which stands for Constant Maturity Treasury. The U.S. Treasury publishes this rate, and it reflects yields on government securities across various maturities. When Treasury yields move up or down, the CMT moves with them.

The lender adds a fixed margin on top of the CMT to arrive at the borrower’s actual interest rate. That margin locks in at closing and doesn’t move. The CMT index itself does move, adjusting monthly or annually depending on the loan terms.

You don’t need to track the CMT daily as a REALTOR. But knowing the term lets you speak fluently with lender partners and field basic questions from clients. When a borrower asks why their rate might change over time, you can point directly to the CMT index as the variable piece.

One point worth emphasizing: rate movement doesn’t change the payment situation. The HECM for Purchase still requires no monthly mortgage payment regardless of where the CMT index travels.

The Role of Mortgage Insurance Premiums

Another cost accrues on the loan balance alongside interest: the FHA mortgage insurance premium, or MIP.

FHA charges two types of MIP on a HECM. An upfront premium hits at closing. An ongoing annual premium then accrues on the loan balance each month, working similarly to interest.

Many borrowers initially view MIP as a cost that benefits only the lender. That framing misses the point. MIP funds a protection called the non-recourse guarantee, and that guarantee works entirely in the borrower’s favor.

Here’s what it delivers. If the loan balance eventually grows larger than the home’s value at the time of sale, the borrower and their heirs owe nothing beyond what the home brings on the market. FHA’s insurance absorbs the shortfall. No one chases the family for the difference.

That guarantee matters enormously to borrowers who worry about leaving debt behind for their children. It also matters to adult children who assume they might inherit a financial burden. The FHA insurance exists precisely to prevent that outcome.

How the Interest Rate Affects Buying Power

Here’s where interest rates connect directly to your job as a REALTOR.

The rate affects the principal limit (your client’s “loan ceiling”), which determines the maximum amount the HECM contributes toward the purchase. A lower rate generally produces a higher principal limit. A higher rate generally produces a lower one.

For a HECM for Purchase buyer, a higher principal limit means they bring less cash to closing from their own funds. A lower principal limit means they need more.

That directly shapes what price range your senior client can realistically target. When rates sit lower, buying power with a HECM for Purchase strengthens. When rates climb, the math shifts and the buyer may need to adjust their target price or increase their down payment.

This makes staying in close contact with experienced HECM lender partners genuinely valuable. A lender who regularly closes HECM for Purchase transactions can help you and your client understand what the numbers actually support given current rate conditions.

What Interest Works When the Loan Ends

When the home eventually sells, or the last borrower permanently leaves, the accumulated loan balance gets repaid from the sale proceeds.

If the sale price exceeds the loan balance, the remaining equity belongs to the borrower or their heirs. That equity can be meaningful, especially when the home appreciated over the years the borrower lived there.

If the sale price falls short of the loan balance, FHA’s insurance covers the gap. The borrower and their heirs walk away owing nothing beyond what the home sells for. The non-recourse protection holds regardless of how large the balance has grown.

Heirs often carry a quiet fear that a reverse mortgage will saddle them with debt they can’t pay off. Helping your clients and their families understand how the loan actually ends removes that fear and builds confidence in the decision. That’s another way you add value as a trusted professional.

Talking About Interest With Your Senior Clients

You don’t hold a HECM lender license. You don’t work as a HUD-approved housing counselor. You don’t need to fill either role.

Your job: recognize when a senior buyer might benefit from exploring a HECM for Purchase, point them toward the right professionals, and help them understand enough to ask good questions.

A few things you can say with confidence:

- “Interest accrues on the balance each month, but the loan requires no monthly mortgage payment.”

- “The rate adjusts over time based on a U.S. Treasury index called the CMT.”

- “If the balance ever grows larger than the home’s value at sale, FHA insurance covers the difference. Your heirs won’t owe the gap.”

- “Before you can move forward, a HUD-approved housing counselor will walk you through all of this in detail. Federal law requires that session.”

That last point deserves extra attention. HUD-approved housing counseling isn’t optional. Every HECM borrower must complete it before moving forward. Encouraging your clients to schedule that session doesn’t overstep your role. It moves the process forward and protects your client.

Three Things Worth Carrying With You

Here are the three points most worth remembering about how interest works on reverse mortgages after reading this.

First, interest accrues monthly but no payment is required. The balance grows rather than shrinks, and that trade-off drives the whole program.

Second, the rate adjusts based on the CMT index plus a lender margin, and it directly determines how much the HECM contributes toward the purchase price.

Third, FHA mortgage insurance protects the borrower and their heirs from ever owing more than the home brings at sale.

Those three points won’t make you a HECM expert. But they will make you a more confident, more credible advocate for your senior clients, and that reputation builds the kind of referral business that compounds over time.

For more resources on the HECM for Purchase and how to grow your business serving senior buyers, visit HECMCoach.com or reach out directly to learn about consulting services, speaking engagements, and continuing education content built specifically for real estate professionals. In the meantime, download our infographic on how interest works with reverse mortgages.

This post was written by the founder of HECMCoach.com, a HUD-certified and HECM-certified housing counselor and Accredited Financial Counselor (AFC) through AFCPE. The information in this post is educational and does not constitute financial or legal advice nor does it represent the views of the writer's employer. Readers should consult a licensed mortgage professional and a HUD-approved housing counselor with a HUD-approved housing counseling agency for guidance specific to their situation.

{kind=link}